##introduction

This company is mainly famous for its communication modules. For anyone with a bit of interest in computers, this name is familiar to the router's processor. It is mainly used in high-end routers. (Not necessarily, but Realtek is mainly used in low-end products.)

At some point, such companies become AI-related stocks. Even looking at securities company reports or company introductions (Namu Wiki, etc.), there doesn't seem to be any products directly related to AI.

So why is it being categorized as an AI theme and in the spotlight?

##Investment point 1. ASIC semiconductor (AI semiconductor)

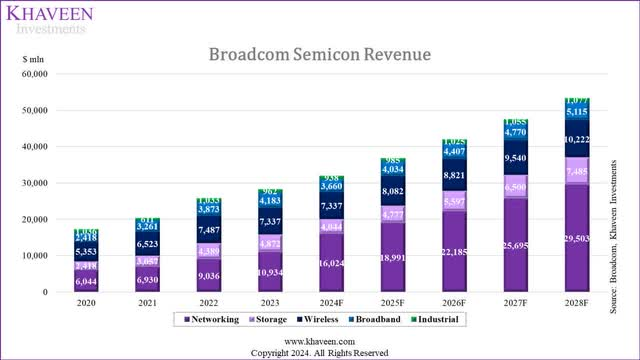

The reason this company is attracting attention is because of its ASIC, customized semiconductor division. Broadcom supplies customized artificial intelligence processor chips (TPUs) to Google, Microsoft, and Meta Platforms, which account for a large portion of its sales. Broadcom's President and CEO Hock Tan disclosed that about 20% of semiconductor sales are coming from AI-related fields, which he said will reach $4 billion in 2024, or 25% of semiconductor sales

(Source: KHAVEEN investment, seeking alpha)

Even if it is not just a company CEO's rant, it is a known fact that the AI semiconductor market is heating up. Even as Nvidia's AI chip costs $15,000, the price is expected to continue to rise. Google's AI chip is known to cost between $2,000 and $3,000. However, it will be difficult to immediately internalize NVIDIA's quality, quantity, and AI semiconductor solution capabilities, and this may be an opportunity for Broadcom. In the future, as a field in which astronomical amounts of money are expected to be invested, each company's efforts to phase out NVIDIA are expected to continue. This is because it leads to enormous cost savings.

Meanwhile, it is not that difficult to expect an improvement in the performance of Broadcom, which already supplies TPUs to Google, Microsoft, and Meta, and even has its own demand for VMWare.

##Investment point 2. Tight portfolio

No matter how well AI performs, it cannot be an object of investment if there are holes on the other side.

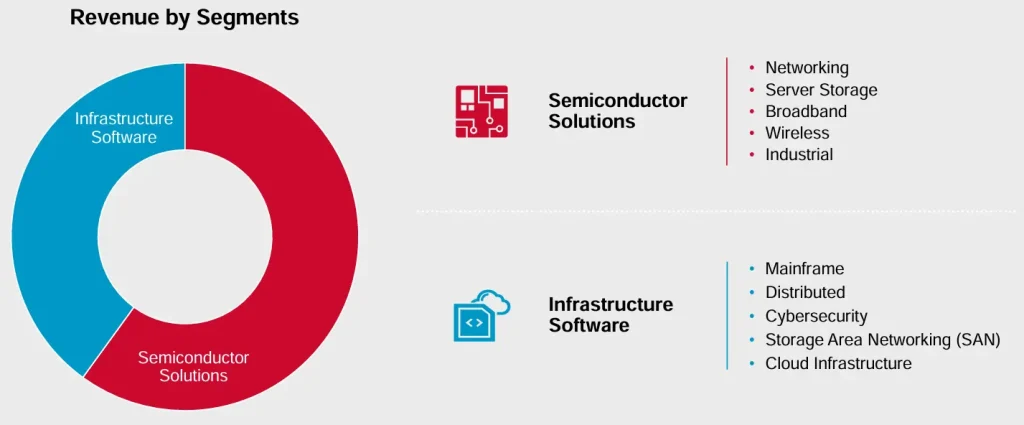

As mentioned briefly earlier, Broadcom has semiconductor-related sales and infrastructure software sales. Looking at the image above (or the presentation material) alone, it can be somewhat misleading, as it does not directly provide services such as networking and server storage, but rather produces related semiconductors. In fact, it covers semiconductors in almost all fields that we simply calladvanced, including networks, big data storage, wireless communications, industrial optics, and motion sensors.

The presence of the infrastructure software sector has also increased with the addition of VMWare, famous for its virtualization software. Using VMWare's products, a single computer or server can be "virtually" divided and utilized, increasing the flexibility of hardware use and making it easy to maintain, making it a technology that is in the spotlight in cloud computing and server operation. VMWare is responsible for approximately 60% of sales in the infrastructure software sector, and is a field expected to grow by more than 20% by 27.

In addition, Symantec, famous for its security solutions, is also expecting high growth of more than 15%, and other sectors such as corporate software and payment security systems are also expected to grow at a good rate of around 5%. In summary, most of Broadcom's business is directly or indirectly tied to the growth of AI, and at least it does not appear to be hindering it.

##Inspection point 1. Valuation

Even if performance is good, stocks must be purchased at a good price. But unfortunately, price is always relative.

In my case, I do not consider valuation to be very important when purchasing stocks. However, check to what extent the stock ranks among similar options in the sector and how far it deviates from the stock's historical levels. The difference from the average can be grounds for a stock to be in the spotlight when your judgment and assumptions are accurate, but it can be a reason for a decline if your judgment and assumptions are wrong.

It's not cheap either. However, if it is a promising stock in a well-performing sector, the price is not prohibitive. Let’s decide based on your own investment strategy and inclination.

ItemBroadcomBroadcom (5-year average) Sector MedianPER (TTM)37.9539.2528.20PER (FWD)34.4434.8627.14PEG (TTM)1.56-1.10PSR (TTM)14.507.332.87PSR (FWD)11.766.842.88PBR (TTM)21.609.053.08PBR (FWD)24.369.624.09Odds (TTM)1.52%2.97%1.50%Source: Seeking Alpha

It's not cheap either. However, if it is a promising stock in a well-performing sector, the price is not prohibitive. Let’s decide based on your own investment strategy and inclination.

##Risk 1. Big Tech chip development itself

There may be room for misunderstanding, so let me point out that for Broadcom, 'getting out of NVIDIA' and big tech's 'internalizing semiconductors' are different concepts. Broadcom, like Nvidia, is a fabless company. To compare it to architecture, it is a company that does design (Fabless) and does not do architecture (Foundry → Samsung Electronics, TSMC). However, while NVIDIA is a company with the know-how to mass-produce ready-made products well suited to AI, Broadcom's main focus is custom semiconductors (ASICs) that are designed in the direction desired by each big tech company. Therefore, the direction that is beneficial to Broadcom is 'getting rid of NVIDIA', not 'internalizing semiconductors'. Broadcom's profits lie somewhere between the explosive growth of the overall AI semiconductor pie and Big Tech's direct design of AI semiconductors. For several years now, big tech companies, including Apple, have been pursuing direct semiconductor design, moving beyond 'post-NVIDIA' ( https://now.k2base.re.kr/portal/issue/ovseaIssued/view.do?poliIsueId=ISUE_000000000001040&menuNo=200&pageIndex=1 ). Open AI became an issue by announcing that it would raise 9,300 trillion won for AI semiconductor development.

Although it turned out to be a rumor, when the news that Google was designing its own TPU, excluding Broadcom came out, the stock price plummeted.

On the other hand, the encouraging part is that Nvidia's dependence is not decreasing even though Big Tech is investing enormous capital. As is the case in all fields, when internalizing outsourced materials or technology, various aspects of efficiency are considered in addition to technology and cost issues.

Although it was designed directly, the high dependence on Google for ASIC sales is also a risk factor. Google's TPU is estimated to account for 75% of Broadcom's ASIC sales.

##Risk 2. Even the customized chips are NVIDIA?

Sadly, there is also news that NVIDIA is entering the ASIC market. Of course, Big Tech's desire to get rid of NVIDIA has a big cost aspect, but as there is a demand for a dedicated design suitable for their own AI logic, there is a possibility that it will encroach on the ASIC market pie. According to data from investment bank Needham, the global custom semiconductor market size is approximately $30 billion in 2023 and is expected to double by 2025. Broadcom's related sales are approximately $10 billion.

##conclusion

At first, I praised it, but towards the end, I wondered if I should buy it or not. As mentioned before, Broadcom's future depends on how quickly the AI market grows and how successful Big Tech's efforts to become self-reliant will be. The future is unknown. Meanwhile, one thing is clear. The AI market will grow at a truly incredible pace. That's it. It is unknown whether Broadcom's share of the huge banquet that AI will prepare will be the main menu or the soybean meal. However, no matter how big or small, it is clear that as of now, it is one of the not bad players in the AI boat.