TSMC maintains an unrivaled position in the market based on its overwhelming technological superiority. Demand in the AI and high-performance computing (HPC) markets is rapidly increasing, and TSMC is taking advantage of this to expand sales and profits. The controversy over Nvidia's high point continues day after day, and its stock price continues to fluctuate significantly. It is unclear whether Nvidia is at its peak or how much further it will rise, but this much seems certain. Demand for semiconductors will continue in the AI era. And high-performance semiconductors go through ‘this company.’ In this article, we learn about TSMC.

main body

TSMC’s Reasonable Growth

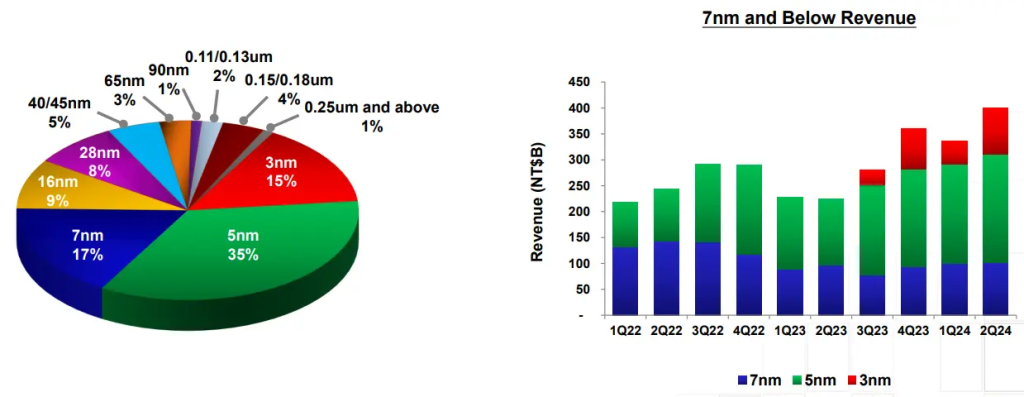

TSMC is expected to continue growing in the second half of 2024 and beyond based on strong demand in the AI and HPC markets. Although the launch was quite late compared to its competitor Samsung, the winner of the 3nm process confirmed over the past year was, without fail, TSMC. Large IT companies such as NVIDIA, AMD, Intel, Qualcomm, MediaTek, Apple, and Google have chosen TSMC, and currently, TSMC's 3nm process sales share reaches 15%. In the case of Samsung, it does not disclose the proportion of sales by process, and although it has already been three years since it announced mass production of the 3nm process, it is known that it has not yet found a suitable major customer..

Source : TSMC Presentation

Source : TSMC Presentation

TSMC seems unwilling to allow even the slightest possibility of catching up. TSMC CEO C.C. In the performance announcement, Wei announced that the 2nm process (hereinafter referred to as N2) is scheduled to enter mass production in 2025, and that mass production of N2P, an improved process of N2, will be introduced in 2026. Compared to N3E, N2 will deliver a 10% to 15% speedup at the same power, or a 25% to 30% power increase at the same speed, and will increase chip density by more than 15%.

Increasing CAPA, rising prices, but undiminished popularity

TSMC is a company that is very adept at strategic pricing, as its reputation as 'Super Eul' suggests. TSMC does not simply set prices based on market conditions, but adheres to 'strategic pricing', which determines prices by considering long-term customer relationships. In particular, as demand for AI and high-performance computing (HPC) rapidly increases, TSMC is planning to increase prices in the 5nm and 3nm processes, and the increase is expected to be approximately 10-20%. TSMC plans to increase its advanced packaging production capacity by approximately 94% to 33,000 pieces (based on wafers) in the third quarter of this year compared to the previous quarter (17,000 pieces).. Nevertheless, demand for advanced packaging is expected to experience a shortfall compared to production next year, and TSMC is expected to actively utilize this position. It is known that TSMC's production contract is already full until 2026.

Foundry 2.0 announces market expansion

TSMC is expanding its market itself through the 'Foundry 2.0' strategy. Foundry 2.0 is not limited to the traditional front-end process (wafer fabrication), but refers to an expanded service range that includes back-end processes (OSAT) such as packaging, testing, and mask production. To put it simply, I'm talking about doing everything except memory.. Through this, TSMC will enter the market worth approximately $250 billion in 2023.

There is also an analysis that the intention is to dilute issues caused by monopoly by expanding the scope beyond the foundry. TSMC's share in the foundry market is 60%, making it a 'monopoly operator' as defined by each country's fair trade laws. However, the combined market share of packaging and testing is around 28%.

conclusion

TSMC is expected to see continued growth in 2024 and beyond based on strong demand in the AI and HPC markets, technology leadership, and close collaboration with customers. Samsung is also aiming to mass produce a 2nm process at the same level as TSMC next year., Intel announces that it will enter the 1nm process, but many analysts believe that the technology gap with TSMC will not easily widen. Even if other companies' cutting-edge processes are commercialized more quickly, TSMC's stock price rally is believed to have sufficient basis, considering the reliability of TSMC's process shown in the 3nm process competition, the number of contracts already accumulated until 2026, and the expansion of the market area due to expansion of production CAPA.

See other posts

3 things to consider before buying NVIDIA (NVDA) (checkpoints and prospects) [[US Stocks] AMD, opportunities come and go (feat. Data Center, Nvidia Related notes)]( https://quokkanews.com/%eb%af%b8%ea%b5%ad%ec%a3%bc%ec%8b%9d-amd-%ea%b8%b0%ed%9a%8c%eb%8a%94-%eb%8f%8c%ea%b 3%a0-%eb%8f%88%eb%8b%a4-feat-%eb%8d%b0%ec%9d%b4%ed%84%b0%ec%84%bc%ed%84%b0-%ec%97%94%eb%b9%84%eb%94%94%ec%95%84/) NVIDIA (NVDA) 2nd quarter earnings release review (Q2) Earnings) [Super Microcomputer, Nvidia-related stock king at the end (AI-related stock, immersion cooling)