Summary

Dell Technologies can no longer be seen as merely a PC manufacturer. As of 2026, the key reason the market is re-evaluating Dell is AI servers. With the expansion of generative AI infrastructure investments, Dell has become one of the primary beneficiaries, supplying NVIDIA GPU-based servers and enterprise infrastructure.

Dell's growth can be seen as evidence that "AI investment is transitioning from semiconductors to actual infrastructure deployment." While the market initially focused on GPU companies like NVIDIA, it is now beginning to look at servers, storage, networking, power, cooling, and operational solutions required to deploy GPUs in actual data centers. Dell stands precisely at this juncture.

Recent earnings were very strong. In the first quarter of fiscal year 2027, the quarter ending May 1, 2026, Dell reported revenue of $43.8 billion, an 88% increase year-over-year. Diluted EPS was $5.24, and non-GAAP EPS was $4.86, increasing by 282% and 214% respectively. Operating cash flow also reached a record high for a first quarter at $4.1 billion.

However, the stock price has risen commensurately. It's time to assess whether it's a structural growth stock, a cyclical stock temporarily riding the AI momentum, and the sustainability of its revenue and profit margins.

What Kind of Company is Dell?

Dell is a global technology company that provides PCs, laptops, servers, storage, networking equipment, and IT infrastructure services. While familiar to general consumers as a laptop and desktop brand, the actual investment focus is more heavily on its enterprise infrastructure business.

Dell's business is broadly divided into two segments:

| Business Segment | Key Activities |

|---|---|

| Infrastructure Solutions Group (ISG) | Servers, Storage, Networking, AI Infrastructure |

| Client Solutions Group (CSG) | Commercial and Consumer PCs, Laptops, Workstations |

Currently, investors are most focused on ISG. This is because demand for high-performance servers, storage, and network equipment is increasing alongside the growing demand for AI data center construction.

It would be a mistake to think of ISG as simply meaning PC cases or server racks. The AI infrastructure referred to by Dell's ISG division encompasses high-density computing, networking, storage, power and cooling, software integration, and lifecycle management. The reason Dell is being re-evaluated as an AI infrastructure integrator is its ability to supply this entire bundle to enterprise customers.

Why Are AI Servers Important?

The AI server value chain can be summarized as follows:

| AI Server Value Chain | Related Content |

|---|---|

| GPU/Accelerators | Core components for AI computation, such as NVIDIA, AMD |

| Memory/Storage | HBM, DRAM, SSD, high-performance file and object storage |

| Server OEM/ODM | Dell, HPE, Supermicro, etc. |

| Networking | Switches, Ethernet, InfiniBand |

| Data Center | Power, Cooling, Racks, Operational Automation |

| Services/Integration | Deployment, Maintenance, Lifecycle Management |

As shown in the table above, Dell's systems handle the final stage of the AI server value chain. In other words, Dell's prominence indicates that AI infrastructure is entering a phase of full-scale growth, and our task is to estimate how far this growth will extend.

Recent Earnings: AI Servers Transformed the Numbers

Dell's Q1 FY2027 earnings can be summarized as "the quarter where AI servers made the company look like a growth stock again."

| Item | Q1 FY2027 | YoY Change |

|---|---|---|

| Revenue | $43.8 Billion | +88% |

| Operating Income | $3.66 Billion | +214% |

| Net Income | $3.44 Billion | +256% |

| Diluted EPS | $5.24 | +282% |

| Non-GAAP EPS | $4.86 | +214% |

| Operating Cash Flow | $4.08 Billion | +46% |

| Adjusted Free Cash Flow | $3.17 Billion | +42% |

The Infrastructure Solutions Group's growth was particularly dominant.

| ISG Details | Revenue | YoY Change |

|---|---|---|

| AI-Optimized Servers | $16.1 Billion | +757% |

| Traditional Servers & Networking | $8.5 Billion | +92% |

| Storage | $4.3 Billion | +8% |

| Total ISG | $29.0 Billion | +181% |

Dell achieved $16.1 billion in AI server revenue in Q1, with new AI server orders totaling $24.4 billion. This means new orders exceeded revenue. It's still too early to be surprised. As of the end of the quarter, the backlog of AI server orders not yet delivered to customers amounted to $51.3 billion.

This demonstrates that AI infrastructure demand is being proven not merely by expectations, but by explosive actual performance.

FY2027 Guidance: Growth Expectations Have Increased

Dell significantly raised its full-year FY2027 revenue outlook.

| Item | Company Guidance |

|---|---|

| FY2027 Revenue | $165 Billion - $169 Billion |

| Revenue Guidance Midpoint | $167 Billion |

| YoY Growth Rate (Midpoint) | Approx. +47% |

| FY2027 AI-Optimized Server Revenue | Approx. $60 Billion |

| FY2027 GAAP EPS Midpoint | $17.31 |

| FY2027 Non-GAAP EPS Midpoint | $17.90 |

The implication of this guidance is clear. Dell's management believes that AI server demand is likely to continue throughout at least fiscal year 2027, rather than being a one-time special event.

Dell's Performance Reflects the AI Market Sentiment

Dell's performance is not an isolated event for a single stock. In essence, Dell serves as the de facto final gateway for "server infrastructure," providing evidence that AI-based equipment, including GPUs, DRAM, servers, storage, and networks, is increasing as a physical entity within "data centers."

Dell Stock Trend (Last 3 Months), StockForum

The approximately 33% surge in Dell's stock price on the day of the earnings release was not simply because revenue and EPS exceeded consensus. It was due to revenue exceeding expectations, meaning that despite significant shipments of AI servers, the order backlog actually increased.

Unlike capital markets, which fear the peak of infrastructure investment amid "AI cycle peak" theories, actual demanders are still busy investing in infrastructure.

Investment Point 1: AI Server Demand Confirmed by Performance

While there are many AI-related stocks, not all companies have demonstrated AI benefits through actual revenue and profit. Dell's advantage is that AI demand is already reflected in its financial statements.

AI server revenue of $16.1 billion, AI orders of $24.4 billion, and an annual AI server revenue forecast of $60 billion all indicate that Dell is a direct beneficiary of the AI infrastructure investment cycle.

Dell, in particular, has a strong enterprise customer base. When companies seek to build their own AI infrastructure or create private AI environments, Dell can provide a bundled solution including servers, storage, networking, and services. This is a strength that differentiates it from mere component suppliers.

The demand base is also expanding. Since early 2026, the usage of Agentic AI has surged, leading to increased demand for on-premise AI from neo-cloud providers, national-level sovereign AI initiatives, enterprise customers for whom security and data control are crucial, and even personal local AI. For Dell, this expansion of the customer base is a critical factor in assessing the sustainability of the AI server cycle.

Investment Point 2: Still Robust PC Business

While AI servers are indeed the most spectacular growth driver, Dell's PC business also provides solid support. In Q1 FY2027, Client Solutions Group revenue increased by 17% year-over-year to $14.6 billion.

| CSG Details | Revenue | YoY Change |

|---|---|---|

| Commercial PCs | $13.0 Billion | +18% |

| Consumer PCs | $1.6 Billion | +9% |

| Total CSG | $14.6 Billion | +17% |

The PC market is not a high-growth industry, but when enterprise replacement demand aligns with the AI PC trend, it can serve as a stable source of cash generation to a certain extent. For Dell, if AI servers are the growth engine, the PC business acts as a foundational support for its business portfolio.

Investment Point 3: Cash Flow and Shareholder Returns

Dell has not only demonstrated growth but also improved its cash flow. Total adjusted free cash flow for FY2026 was $11.5 billion, and for Q1 FY2027, it was $3.17 billion.

Furthermore, Dell returned $2.1 billion to shareholders in Q1 FY2027 through share repurchases and dividends.

| Item | Amount |

|---|---|

| FY2026 Adjusted Free Cash Flow | $11.5 Billion |

| Q1 FY2027 Adjusted Free Cash Flow | $3.17 Billion |

| Q1 FY2027 Shareholder Returns | $2.1 Billion |

| Q1 Share Repurchases | $1.63 Billion |

| Q1 Dividends and Dividend Equivalents Paid | $0.46 Billion |

The trend of shareholder returns continued after the earnings announcement. On June 16, 2026, Dell declared a quarterly cash dividend of $0.63 per share of common stock, with a payment date of July 31, 2026.

In a situation where its growth stock characteristics have strengthened, the combination of strong cash flow and shareholder returns can be viewed positively by investors.

The key point to observe here is that while AI servers may put pressure on gross profit margins, an increase in revenue scale can lead to a reduction in the operating expense ratio. Indeed, in Q1 FY27, the gross profit margin decreased due to the AI server mix, but the operating profit margin improved. Dell's investment appeal ultimately depends on how well it can convert "increased low-margin hardware revenue" into "operating leverage and cash flow."

Valuation: Neither Cheap Nor Excessively Expensive

When evaluating Dell's valuation, the interpretation differs depending on whether it is viewed as a traditional PC hardware company or an AI infrastructure growth stock.

| Item | Value | Basis / Calculation |

|---|---|---|

| Stock Price | $409.50 | As of June 18, 2026 |

| Market Cap | Approx. $268.6 Billion | As of June 18, 2026 |

| TTM P/E | Approx. 32.6x | Based on trailing 12-month earnings |

| FY227 Non-GAAP EPS Guidance | $17.90 | Company-provided midpoint |

| Forward P/E | Approx. 22.9x | $409.50 / $17.90 |

| FY2027 Revenue Guidance | $167 Billion | Company-provided midpoint |

| Forward P/S | Approx. 1.6x | Market Cap / Revenue Guidance |

Viewed as an AI infrastructure growth stock, a forward P/E in the low 20s and a forward P/S in the mid-1s are not necessarily considered excessively high. However, it is quite unusual for Dell, a company closer to a simple PC maker or even general manufacturing with existing replacement cycles, to be treated as a growth stock.

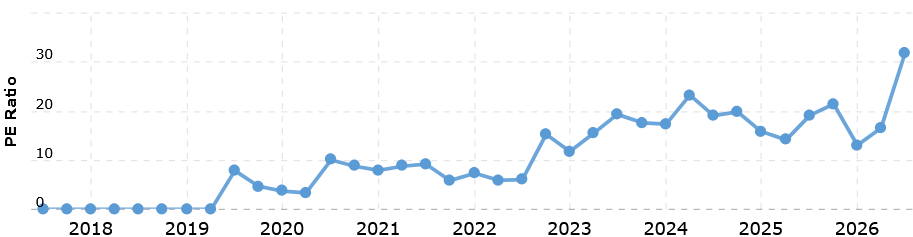

2017~Present DELL PER Trend, Macro Trend

The P/E trend alone confirms this. The current P/E exceeding 30 is an overwhelming level, unseen even during the Cloud cycle. This means it's crucial to recognize that the current Dell stock price already reflects expectations of "sustained AI server growth" and to closely monitor market expectations versus actual AI performance. A significant portion of expectations has already been priced in. For the stock price to rise further, simply increasing revenue will not be enough; the profitability of the AI server business must also improve.

Key Risk 1: Margin Pressure

Dell's gross profit margin for Q1 FY2027 was 17.8%, lower than 21.1% in the prior-year quarter. While revenue grew explosively, AI servers have high costs for GPUs and high-performance components, and competition is fierce.

| Item | Q1 FY2027 | Prior-Year Quarter |

|---|---|---|

| Gross Profit Margin | 17.8% | 21.1% |

| Non-GAAP Gross Profit Margin | 18.1% | 21.6% |

| Operating Profit Margin | 8.3% | 5.0% |

| Non-GAAP Operating Profit Margin | 9.7% | 7.1% |

As mentioned earlier, the foundation of Dell's business is the PC business, and the essence of the AI server business is also the same: "component procurement → server configuration → delivery and after-sales service." Therefore, it is a business with limitations in securing margins.

Consequently, despite tremendous performance growth and order announcements, the gross profit margin decreased from 21.1% in the prior-year quarter to 17.8%. Of course, this could also be partly due to the inability to pass on all rapidly rising component costs to customers, so this is an area that needs continuous monitoring.

Key Risk 2: Potential Slowdown in AI Investment Cycle (+Customer Concentration)

Unfortunately, the market does not allow a late-starting rally to last longer. Dell's current performance heavily relies on the expansion of AI infrastructure investment. If major customers temporarily reduce AI server investments or enter a phase of monetizing their existing infrastructure, Dell's growth rate is likely to slow, and its stock price could react proportionally faster. In particular, AI server demand is likely to be driven by large-scale orders from hyperscalers. AI servers can only be delivered when GPUs, memory, networking equipment, and cooling solutions all align. A bottleneck in any of these could affect revenue recognition speed and margins.

Key Risk 3: Supply Chain and Customer Concentration

AI servers can only be delivered when GPUs, memory, networking equipment, and cooling solutions all align. A bottleneck in any of these could affect revenue recognition speed and margins.

| Risk | Point to Monitor |

|---|---|

| GPU/Memory Supply Bottleneck | Orders may be high, but deliveries could be delayed |

| Rising Component Prices | Need to confirm if price increases can be passed on to customers |

| Contract Price Adjustment Disputes | Price and delivery issues in large server orders could escalate into legal disputes, as seen in the XTX case |

| Demand Driven by Large Customers | Quarterly performance volatility could increase |

| Backlog Conversion Rate | Confirm if orders are translating into actual revenue and profit |

| Storage/Service Attach | Confirm if it can complement low-margin server revenue |

Dell has strong cash flow but also significant debt. As of May 1, 2026, cash and cash equivalents were $11.58 billion, and the sum of short-term and long-term debt was approximately $31.16 billion.

Key Risk 4: Significant Debt

Dell has strong cash flow but also significant debt. As of May 1, 2026, cash and cash equivalents were $11.58 billion, and the sum of short-term and long-term debt was approximately $31.16 billion.

| Item | As of May 1, 2026 |

|---|---|

| Cash and Cash Equivalents | $11.58 Billion |

| Short-Term Debt | $7.55 Billion |

| Long-Term Debt | $23.61 Billion |

| Total Short-Term + Long-Term Debt | $31.16 Billion |

| Total Assets | $114.91 Billion |

| Total Liabilities | $116.32 Billion |

Fortunately, Dell's strong cash-generating capability mitigates its debt burden. However, the interest rate environment, refinancing costs, and working capital requirements related to AI servers must be continuously monitored.

Checkpoints

Key metrics to keep in mind when looking at Dell are as follows:

| Checkpoint | Why It's Important |

|---|---|

| AI Server Revenue Growth Rate | Core growth engine for Dell's investment story |

| AI Orders and Backlog | To assess revenue visibility beyond the current quarter |

| Gross Profit Margin | To confirm if AI servers are translating into actual profit |

| ISG Operating Profit Margin | To assess the profitability of the infrastructure business |

| Adjusted Free Cash Flow | To assess the sustainability of growth and shareholder returns |

| Scale of Shareholder Returns | To check capacity for share repurchases and dividends |

| Debt and Interest Expense | To review financial risks |

| Customer Diversification | To confirm expansion beyond hyperscalers to neo-cloud, sovereign AI, and enterprise |

| Storage/Service Attach Rate | To confirm if AI server revenue leads to higher profitability |

Conclusion: Dell is a Proven Beneficiary of AI Infrastructure

Dell can no longer be seen as merely a cyclical PC stock. It is a direct beneficiary of the AI infrastructure supercycle, supported by revenue growth, EPS growth, cash flow, and shareholder returns. As of 2026, Dell's investment story hinges on how long and with what margins AI server revenue can be sustained.

As seen in the recent XTX price dispute, the core of investing in Dell is clear: Will AI investment continue? And can stable margins be maintained?

Rather than chasing the stock during a sharp rise after earnings announcements, new investors would be more rational to adopt an approach that confirms whether AI server revenue growth and gross profit margins are improving together, whether the backlog is converting into actual revenue and cash flow, and whether the company's earnings power is growing enough to sustain the AI infrastructure premium granted by the market.

References

- Dell Technologies, 2027회계연도 1분기 실적 발표, 2026년 5월 28일

- Dell Technologies, 2026회계연도 연간 실적 발표, 2026년 2월 26일

- Dell Technologies SEC Form 8-K, 2027회계연도 1분기 실적 자료: https://www.sec.gov/Archives/edgar/data/1571996/000157199626000021/exhibit991earnings8kq1fy27.htm

- Dell Technologies Investor Relations: https://investors.delltechnologies.com/

- Dell Technologies Stock Information, 2026년 6월 18일 종가 및 배당 이력 확인: https://delltechnologies.gcs-web.com/stock-information

- Dell Technologies, "Dell Technologies Declares Quarterly Cash Dividend", 2026년 6월 16일, 확인일 2026년 6월 19일: https://investors.delltechnologies.com/news-releases/news-release-details/dell-technologies-declares-quarterly-cash-dividend-12

- The Irish Times, "Dell sued by Finnish company over $70m price increase for data centre servers", 2026년 6월 15일, 확인일 2026년 6월 19일: https://www.irishtimes.com/crime-law/courts/2026/06/15/finnish-company-sues-dell-over-70m-price-increase-for-data-centre-servers/

- Financial News, "XTX Markets sues Dell over $619m data centre bill", 2026년 6월 16일, 확인일 2026년 6월 19일: https://www.fnlondon.com/articles/xtx-markets-sues-dell-over-619m-data-centre-bill-4c0345d2

- Seeking Alpha News, "What's next for Dell stock after record-breaking AI results?", 2026년 6월 4일, 확인일 2026년 6월 19일: https://seekingalpha.com/news/4600751-whats-next-for-dell-stock-after-record-breaking-ai-results

- MarketWatch, DELL 실적 후 주가 반응 및 52주 고점 관련 보도