NVIDIA 2nd quarter performance summary

- NVIDIA's sales increased 101% compared to the second quarter of the previous year, and guidance for the third quarter predicted explosive growth of $16 billion.

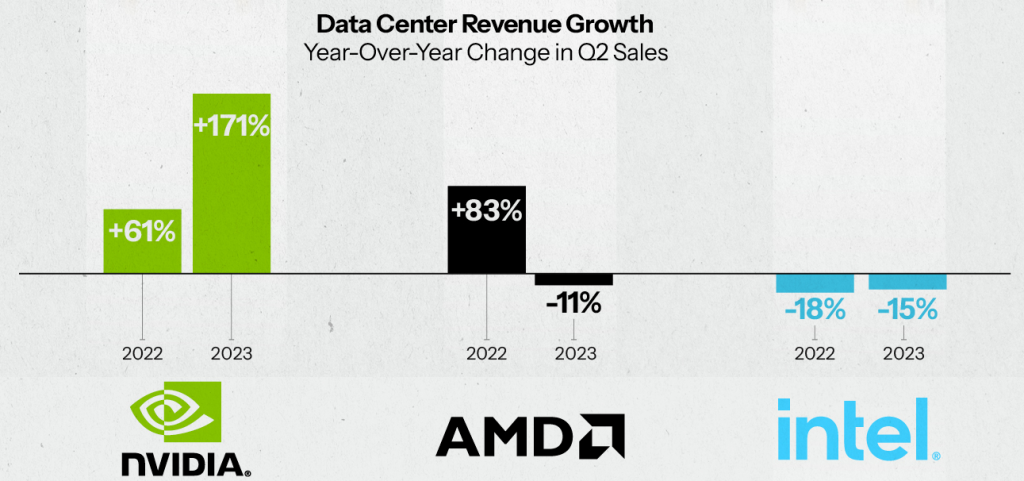

- This performance was thanks to the tremendous growth of data centers, with performance reaching $10.32 billion, a 171% increase over the previous year.

- The gaming segment grew by 11%, showing recovery from the slowdown, and the high-performance graphics segment also grew by 28%.

- However, automobile-related sales decreased by about 15% due to sluggish demand from China.

- $25 billion worth of stock buybacks announced a quarterly dividend, albeit a small one (4 cents).

**Performance Review 1. Once again, AI, data center**

Data center revenue by segment increased 171% from the previous year to $10.3 billion, a truly remarkable achievement. It was a sufficient number to boost the automobile division, which was relatively sluggish, and the gaming and high-performance graphics division, which performed well. Most of the revenue growth next year is expected to be led by the data center division, and for reference, this quarter's data center sales account for 77% of total sales.

The cause appears to be the explosive demand for AI, represented by Chat GPT. The scope of AI's activities is no longer limited to the level of assisting the cloud or programs used by some experts, such as graphics, programming, and creation. Many people are already getting used to getting help or getting quick results through search engines or web pages. People feel greater satisfaction than before with non-face-to-face customer consultation services that have been replaced by AI, and they also prefer or pay for various educational, editing, and cloud applications that add AI.

As proof of this, most large Internet companies are sparing no effort in investing in AI. As an example, Meta Platforms (META) even reduced its capital spending on servers this year while increasing its investment in AI servers..

Performance Review 2. Maybe it's still underrated? (Guidance)

NVIDIA's tremendous performance and guidance announced this time showed that NVIDIA's strong performance was not just a one-time bubble. As if to represent this, after the announcement, Nvidia's stock price soared more than 6%, while AMD's stock price fell by about 8%. NVIDIA's operating leverage based on its solid market dominance and high margin structure reflects expectations that it will create a virtuous cycle that will once again solidify its market dominance. The actual performance changes of the three data center semiconductor companies also reflect this.

Data center sales trend (Source: Visual Capitalist, edited version)

Data center sales trend (Source: Visual Capitalist, edited version)

NVIDIA's Forward PER (based on Yahoo Finance on 8/28) is 46.51, AMD 37.17, and Intel 59.52, which is not particularly high compared to the peer group. Rather, it was once mentioned in Previous article on optimal stop loss Mark Minervini, a well-known trading expert, said that stocks that rose based on performance often had a PER around 60. There is an opinion that the high PER of high-growth stocks is evidence of a lot of people's interest in them.

Looking at the EPS forecast, which has been continuously updated upward since Nvidia's earnings announcement, the PEG indicator, which Peter Lynch, famous for investing in undervalued growth stocks, emphasized, is also 1.56 based on Yahoo, and if the current trend continues, it will soon fall below 1.5. According to traditional value investment standards, the current PER exceeding 100 could be the basis for overvaluation, but it does not seem to be so high that it cannot be digested even if it grows according to the guidance announced this time.

Performance Review 3. The economic moat will become increasingly solid.

NVIDIA's next-generation technology, the Hopper architecture, is represented by the H-100 GPU and Grasshopper GPU. The H-100 GPU is a powerful AI-centric GPU designed to process deep neural networks (DNN) in areas such as autonomous vehicles, robotics, medical care, and life sciences. Grasshopper GPU, another lineup, is a general-purpose GPU that surpasses the existing RTX series and is said to be specialized in graphics implementation and optimized for running creative applications such as games and simulations. The GH200 system, scheduled to be released in 2024, will integrate the above two technologies and provide a large-scale AI development environment that integrates as many as 256 GPUs and shares 144 tera of GPU memory. There is already a huge demand for these chips, and it is expected to accelerate further with the introduction of the GH200 system in the future.

It is not just a technological gap. NVSwitch and NVLink technologies, which are also used in the GH200, enable the configuration of high-performance supercomputers by combining and expanding products, but the use of NVIDIA's unique technology naturally makes it difficult to utilize chips from other manufacturers. Of course, competitors will also support similar features, and in some cases, they may be superior, but it will not be easy to push out an already established super computer. Moreover, even when individuals replace their smartphones, we often choose existing brands due to our lingering feelings about Apple or Google Cloud. This applies not only to hardware but also to software developers. Depending on which manufacturer's hardware and platform is used, the development direction and implementation method of the same function differs. Therefore, it is highly likely that developers will continue to prefer Nvidia's products, which are already dominating the current market (even if costs increase).

Nvidia's development partnership with AstraZeneca (AZN), well known to us for its coronavirus treatment, can be an example. This partnership is a generative AI development study for chemical structure research of new drugs, provided to researchers and developers through NVIDIA NGC software, and can be distributed on the NVIDIA Clara Discovery platform. In addition, various studies, such as the medical language model GatorTron, are being conducted through NVIDIA's platform or hardware. As such research data accumulates, NVIDIA's technical and psychological moat increases.

conclusion

This is a company that would be a waste to filter out simply by looking at value indicators. Of course, the macroeconomic and international situation (ex. China) is not easy, but at least the current high demand and growth for AI semiconductors is expected to continue.