outline

Coupang has become one of the indispensable companies for Koreans, so much so that it is no exaggeration to say that it is now essential. There are reports that Coupang is on the verge of an annual surplus for the first time this year.

In this article, we will look into the investment points of Coupang (ticker: CPNG), which is listed in the United States.

Investment point 1. Transforming into a profitable company

Just a year or two ago, Coupang was a company that was used as a basis for ridicule of SoftBank Chairman Masayoshi Son due to its continuous deficit of hundreds of billions of won every year. However, Coupang is already on the verge of its first annual surplus. The operating profit surplus continued for four consecutive quarters, and operating profit increased by a whopping 42% compared to the previous quarter, reaching an all-time high of KRW 136.2 billion. Net profit also increased to KRW 190.8 billion compared to the previous quarter, putting the company on the verge of an annual surplus. Continuing from last year, Coupang continues to see sales growth of more than 20% year-on-year every quarter this year.. Considering the sluggish performance of giant companies such as Amazon (11%), Alibaba (9.7%), JD.com (4.6%), and Walmart (4.4%), this is a growth that stands out.

Many people dream of explosive growth of hundreds or thousands of times in the future and consider investing in growth stocks or startups that are making large losses, but it is not too late to invest in real growth stocks in the year when they start to make a profit. Tesla is a prime example. Tesla was a company where even rumors of bankruptcy were frequent until it turned profitable in 2020. Tesla's stock price soared from around $30 in January 2020, when it turned into a surplus, to over $400 in November 2021, and is still around $220 after adjustment. Of course, before 2015, the stock was less than $10, so if you could buy it cheaper, you could have made a bigger profit, but considering the hearts of the few who endured that long period of time worrying about bankruptcy, let alone a loss, the profit of more than 10 times after turning into a surplus is truly grateful. Anyway, if Coupang is a real growth stock, now may be an opportunity.

Investment point 2. Formation of an economic moat

In addition to profitability, Coupang appears to have succeeded in building an economic moat, at least in the domestic E-commerce market. Over the years, Coupang has endured huge losses and built more than 100 fulfillment centers handling millions of products. Coupang is close to a complete company in quick commerce, to the extent that it has been said that more than 70% of the country's population lives within 10km of the Coupang logistics center even a year or two ago.

We are also active in using AI and machine learning to differentiate ourselves from competitors. Coupang has been actively utilizing the latest technology, including algorithms that optimize the logistics system, such as predicting order quantities and placing products in logistics centers in advance, as well as optimizing the movement of products within the warehouse through AI. The 24-hour customer center using AI is so effective that the customer satisfaction rate is close to 90%.

Of course, companies with considerable capital, such as Naver, Shinsegae, G Market, and 11th Street, will continue to invest to keep Coupang in check, but Coupang has already gone through such times and is moving forward again.

Investment point 3. Still ample expansion potential

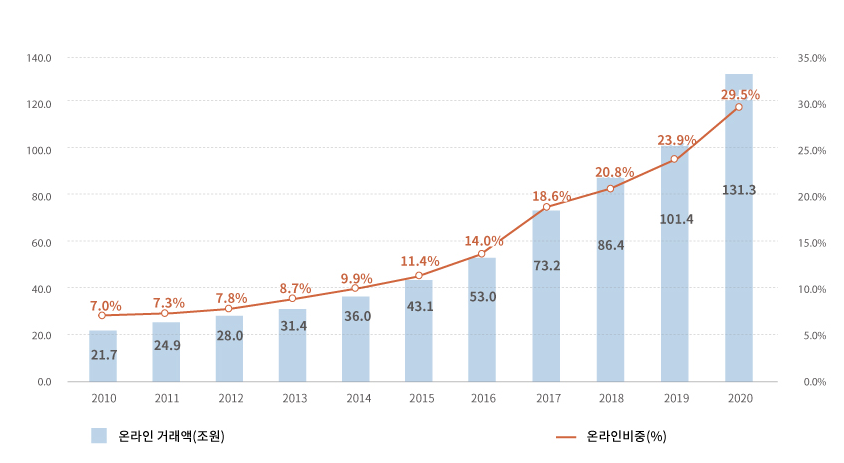

I don't think there will be much room for growth now, to the point where I wonder if there are any Koreans who don't still use Coupang, but it's too early to predict. According to InvestKorea, Korea's e-commerce sales are 29.5% of the entire retail market as of 2020.

Korean retail online transaction volume, transaction proportion (Source: InvestKorea)

Korean retail online transaction volume, transaction proportion (Source: InvestKorea)

This growth slowed down after the resumption of COVID-19, but has recently been improving again. The purchasing power of a generation well-versed in online use is continuously increasing, and a culture that finds it difficult to meet face-to-face, increased social anxiety due to random crimes, and a tendency to avoid going out due to abnormal weather appear to be favorable factors for the expansion of the E-commerce market. According to Mordor Intelligence, considering inflation, Korea's retail market is expected to continue to grow by more than 4.5% over the next five years.. Moreover, Coupang has no intention of simply remaining the number one online shopping company. In the first quarter 2023 earnings announcement, Coupang founder Kim Beom-seok, former director, said the following.

We still maintain a single-digit share of the overall market. The overwhelming majority of the retail market is brick-and-mortar, with expensive prices and limited choices. We're excited about the opportunity to wow our customers with greater selection, lower prices and exceptional service to continue capturing significant growth. (1Q23 performance announcement)

The 'giant distribution market' in the statement refers to everything including dining out and travel, and according to Euromonitor, a global market research company, the size of the domestic distribution market is around 602 trillion won. Considering Coupang's sales level, its market share is estimated at around 4.4%. The market that Coupang sees is vast, and market development is just the beginning.

Investment point 4. Business diversification (Coupang Eats, Fresh, Play)

As all Koreans already know, Coupang’s competitiveness is truly overwhelming. From product search to ordering and payment, there is no unnecessary hassle. Product recommendations that capture my heart every time I open the app constantly tempt users and are even annoying. Based on this, Coupang has successfully increased the number of members signing up for the WOW service, and customers who use it are also taking this for granted. Coupang is slowly shifting its stance aggressively in areas other than E-commerce based on WOW members.

In particular, Coupang Eats’ progress is notable. Coupang recently began offering free shipping and discounts to WOW members. Based on the growing profits from Coupang E-commerce, the company began to actively invest in other fields. In regions where these benefits were launched, the number of WOW members using Coupang Eats increased by 80%, and the average amount of money WOW members spend on Eats increased by 20%.

According to founder Kim Beom-seok, the majority of WOW members do not yet use Coupang Eats, and Coupang Eats benefits for WOW members will continue as regular benefits. It is expected that Coupang Eats will continue to expand its market share.

Investment point 5. Overseas expansion underway (Taiwan)

For Coupang investors, it is also good news that Coupang is increasing its market share in Taiwan. Coupang has had painful experiences with Japan when it comes to overseas expansion, but Taiwan is different from Japan. Japan already had powerful competitors such as Amazon Japan, Rakuten, and Z Holdings (Naver), and due to Japan's geographical characteristics, it had to face enormous costs and severe competition to realize 'quick commerce', which is Coupang's competitive edge.

In comparison, Taiwan's land area is relatively small, but its population density is higher than that of Korea. This is where the advantages of rocket delivery can be maximized. Of course In Taiwan, there are Shopee (SE) and momo that are leading the market., with ample financial power. Taobao and Amazon are also making inroads, but competition is only just beginning as Taiwan's E-commerce market share is still around 10%.

Coupang does not disclose separate performance in Taiwan, but founder Kim Beom-seok said in the last conference call, “Coupang was the most downloaded application in Taiwan in the second quarter and is growing faster than Korea,” and “We plan to continue investing at a high level in Taiwan,” so growth in Taiwan appears to be going smoothly.

Taiwan's e-commerce market penetration rate is around 10%, but is expected to increase from $20.491 billion (about 29.23 trillion won) in 2021 to $28.111 billion (about 40 trillion won) in 2025.

Concluding

So far, we have looked into Coupang’s investment points. As any Korean knows, it is clear that Coupang is a competitive company. In that respect, I think expanding into Taiwan is a good decision, and profitability improvement in various areas such as beauty, fashion, and food and beverages (Coupang Eats, Fresh) is also expected. However, this is an improvement in performance and does not guarantee a rise in stock prices.

According to Yahoo Finance (as of 8/16), Coupang's Trailing PE is 78.88 and Forward PE is 58.48. Some may say that it is undervalued compared to Amazon, but Amazon and Coupang not only have different main target markets, but also have different sales compositions due to the influence of AWS. For reference, Alibaba has already posted PE is at the level of Trailing 20 and Forward 10.

As massive investments will continue in the future to secure competitiveness and enter new markets, it is highly likely that the high PER will continue, at a level where the stock price may fall at any moment, even if the stock price rises with luck.

As with any stock, you must be 'cautious when investing' and this article 'should be used as a reference only', but this is especially true when investing in growth stocks. Let’s make investments based on our own judgment and clear convictions.